The final months of 2025 offered a reminder that some of the most meaningful stretches for investors are not defined by dramatic moves, but by how uncertainty is navigated along the way. As the fourth quarter unfolded, the challenge was less about reacting to any single headline and more about staying grounded as expectations continued to evolve.

The quarter reflected a broader sense of transition. Markets appeared to settle into a more familiar rhythm, even as questions about growth, policy, and the path forward remained unanswered. Although markets often appeared calmer on the surface, underlying uncertainty remained elevated, reinforcing that periods of lower volatility do not necessarily signal reduced risk. For investors, this environment meant balancing optimism with realism and accepting that clarity often arrives gradually rather than all at once. Instead of closing with one single defining moment, the quarter ended with a sense of recalibration.

Our focus has remained on the fundamentals we emphasize most, including thoughtful planning and keeping decisions aligned with long-term goals, even as markets and conditions continue to change. Taking the time to review priorities, revisit goals, and make measured adjustments can be just as valuable as engaging with markets themselves.

While 2025 proved to be a strong year overall, that outcome is never guaranteed. Hindsight helps explain the drivers of performance, but the year ahead will demand the same steady focus and disciplined decision-making to manage whatever comes next.

The record-long U.S. government shutdown extended into the fourth quarter before concluding as lawmakers reached an agreement that included a short-term funding package. This resolution eased near-term policy concerns for financial markets but largely deferred more substantive fiscal negotiations, pushing broader budget and deficit discussions into 2026 rather than resolving them outright.

The shutdown temporarily disrupted the release of key economic data and government operations, and its resolution restored the flow of official economic reporting.

For investors, the end of the shutdown reduced immediate headline risk but did little to resolve longer-term fiscal uncertainty. With attention shifting to rising federal deficits and the increased volume of Treasury issuance required to fund government operations, markets refocused on how fiscal dynamics could influence interest rates and borrowing costs over time. While the shutdown’s direct economic impact appeared contained, its resolution underscored the ongoing tension between short-term stability and longer-term fiscal challenges, which is an issue that is likely to remain relevant as policymakers and markets look ahead.

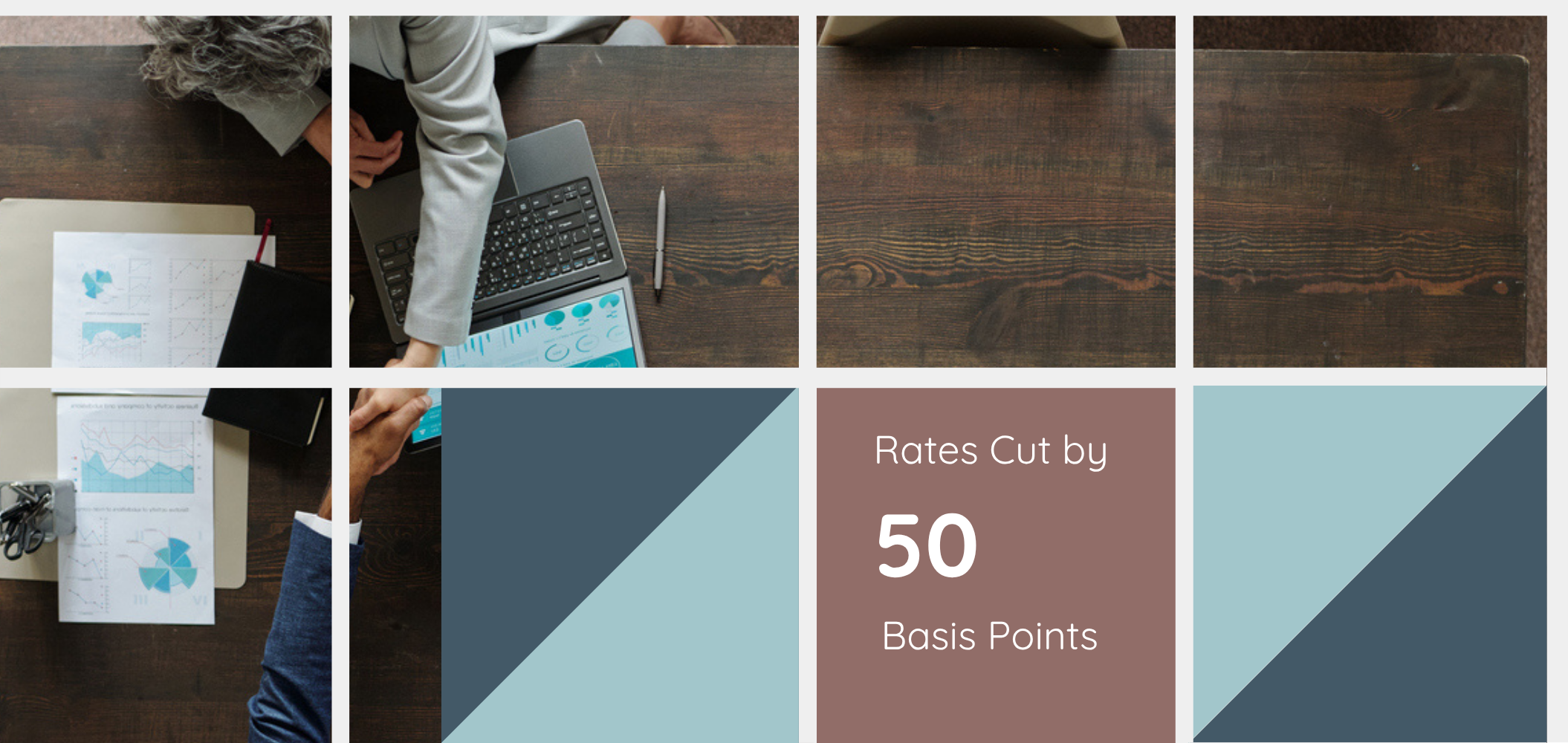

The Federal Reserve lowered its benchmark interest rate in October and December, with cumulative cuts totaling 50 basis points. These moves extended the easing cycle that began earlier in the year, as inflationary pressures continued to moderate and economic growth showed signs of cooling, particularly in interest-rate-sensitive areas of the economy. By late in the quarter, market attention shifted from whether additional cuts would occur and toward how far the easing cycle might ultimately extend into 2026.

The rate cuts reinforced the Fed’s effort to balance sustaining economic momentum with preserving progress on disinflation. As markets generally welcomed the policy shift, the Fed emphasized its data- dependent approach, signaling that future decisions would remain closely tied to incoming economic information rather than a predetermined path. For investors, this environment reflects a transition toward less restrictive monetary policy, though not yet a fully accommodative stance. That distinction remains important for both equity valuations and bond market expectations.

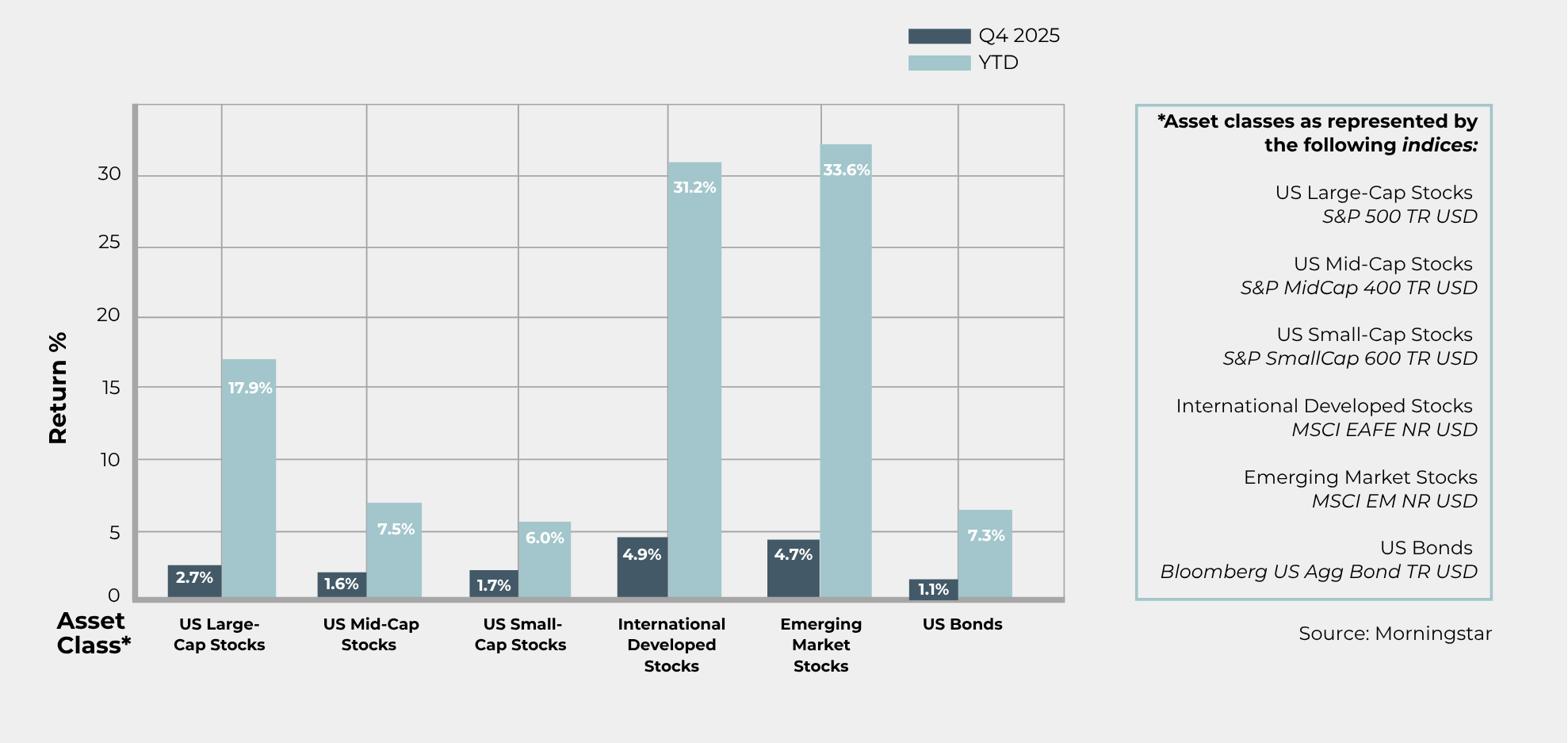

Global economic conditions in the fourth quarter reflected increasing divergence across regions. While the U.S. economy showed signs of cooling, parts of Asia displayed signs of stabilization, and Europe navigated slower but more resilient growth than earlier in the year. The Asia-Pacific Economic Cooperation (APEC) summit held late in the quarter pointed to these contrasts, as several Asia-Pacific economies emphasized growth stabilization, trade coordination, and structural reforms, while the U.S. entered year-end with a greater focus on moderating inflation and managing a softening economy.

Differences in inflation trends, labor market dynamics, policy responses, interest rate paths, and shifts in currency valuations contributed to varied economic outcomes. Diverging growth paths and monetary policies can create dispersion across asset classes, currencies, and sectors, presenting both risks and opportunities. In this environment, diversification across regions and markets remains an important consideration as the global economy transitions into 2026.

Investment in artificial intelligence (AI) infrastructure accelerated across both the private and public sectors. Major technology “hyperscalers” (such as Amazon, Microsoft, Google, and Meta) continued to signal elevated capital spending tied to data centers and AI workloads, with Meta announcing a large-scale financing arrangement in October to support the development of a new AI-focused data center. Meanwhile, the U.S. Department of Health and Human Services released a strategic framework outlining the expanded role of artificial intelligence in healthcare delivery and innovation.

These developments highlighted how AI investment is extending beyond technology companies alone and becoming a broader focus of corporate strategy and public policy. The implications for markets and the economy may prove to be significant. Expanding AI infrastructure requires substantial investment in physical assets, energy, and related supply chains, linking technology growth more directly to commodities and power demand. For investors, sustained commitments by both hyperscalers and public institutions highlight AI’s potential role as a long-term driver of productivity and capital spending, while also introducing considerations around infrastructure capacity, energy usage, and regulatory oversight.

Throughout 2025, investors were reminded that progress rarely unfolds in a straight line. Shifts in monetary policy indicated growing confidence that inflation was moving in the right direction, even as caution remained a central theme. Corporate earnings, consumer behavior, and investment activity pointed to an economy that continued to expand, though at a slower and more selective pace. Globally, economic divergence became more pronounced as regions followed distinct paths rather than moving in lockstep.

Beyond the data, 2025 quietly tested patience and resolve. Investors were asked to process a steady stream of information, sit with uncertainty, and resist the urge to respond to every short-term development. Often, the challenge was less about the markets themselves and more about maintaining perspective in a noisy environment.

The experience of 2025 reinforced an enduring principle: long-term progress can be made through discipline, diversification, and trust in a well-constructed plan. As the year concluded, this environment made ongoing planning, regular portfolio reviews, and alignment with long-term objectives especially important, regardless of short-term market conditions. With uneven regional growth, shifting monetary policy, and episodic geopolitical uncertainty, a diversified approach across asset classes and markets helped reduce reliance on any single outcome. While uncertainty is an inherent part of investing, steady guidance and thoughtful decision-making can help create a sense of confidence and calm, even when the path forward is not perfectly clear.

Broader fiscal negotiations in 2026 are likely to influence confidence in government spending and borrowing.

Lower rates may help keep inflationary pressures in check while supporting continued growth, shaping expectations for future policy decisions.

Diverging trends across regions may influence how U.S. and international markets move relative to one another.

Developments in Venezuela remain an area to watch as geopolitical factors continue to shape energy market conditions.

Insights from Erin Itkoe, President of Luminescent Wealth Management This article was originally published on the Journal of Accountancy website. Link to the full article:

The annual Tax and Legal Seminar brings together Arizona’s leading estate planning attorneys, CPAs, insurance agents, and financial planning professionals for a morning of education

Medicare is a cornerstone of health coverage for millions of Americans age 65 and older (and certain younger individuals with disabilities). But understanding how Medicare

How Arizona taxpayers can redirect state taxes to causes they care about Arizona taxpayers have a unique opportunity to redirect a portion of their state

This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third-party sources and is believed to be reliable; however, its accuracy is not guaranteed and should not be relied upon in any way whatsoever. This presentation may not be construed as investment, tax or legal advice and does not give investment recommendations. Any opinion included in this report constitutes our judgment as of the date of this report and is subject to change without notice.

The index and mutual fund performance shown is presented gross of our advisory fees, trading costs, and other expenses that may be incurred in an actual investment account. This information is provided for illustrative purposes only and does not represent the performance of any specific portfolio or client account. The index returns are not intended to imply or compare to actual portfolio performance and should not be relied upon as an indication of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.