Medicare is a cornerstone of health coverage for millions of Americans age 65 and older (and certain younger individuals with disabilities). But understanding how Medicare premiums are calculated, and why they change each year, can be confusing and costly if overlooked. Below is an explanation of the key components that determine your Medicare costs, along with a summary of the 2025 vs. 2026 premium changes.

At a Glance

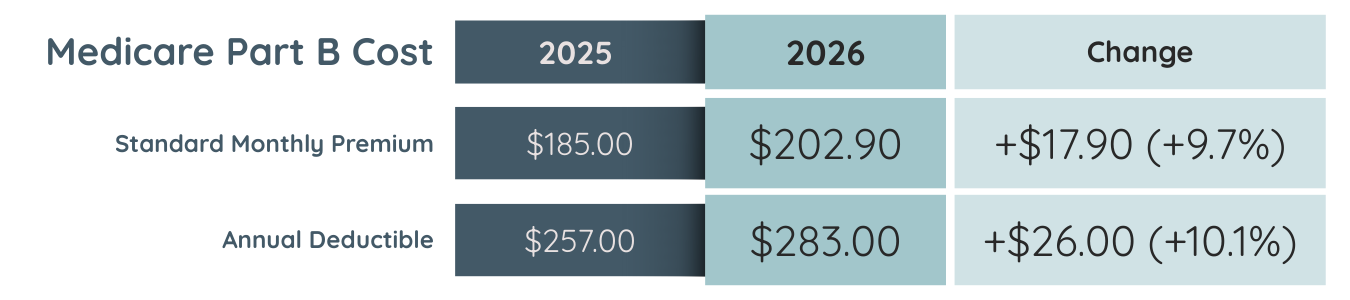

- Standard Medicare Part B premiums increased by nearly 10% from 2025 to 2026.

- Income matters. High-income beneficiaries pay more through IRMAA, based on MAGI from two years prior.

- Premiums are set annually based on expected program costs, utilization trends, and policy factors.

- Higher Part B premiums can potentially reduce net Social Security deposits.

Medicare Premium Basics

Medicare is divided into parts, and each part has its own cost structure:

- Part A (Hospital Insurance):

Most individuals who have worked and paid Medicare taxes long enough (at least 40 quarters), or who are married to (or, in certain cases, were previously married to) someone who meets the Part A requirements, pay no monthly premium for Part A. Those who haven’t met the requirements may pay a premium to receive coverage. Part A also has a deductible and coinsurance for inpatient care. - Part B (Medical Insurance):

Part B covers physician services, outpatient care, durable medical equipment, and certain other services. Almost all beneficiaries pay a monthly premium for Part B.

Standard Part B Premiums and How They’re Set

The standard Part B premium is set each year by the Centers for Medicare & Medicaid Services (CMS) based on the estimated cost of providing Part B benefits. By law, premiums are set to cover approximately 25% of projected program costs, with general revenues and payroll taxes covering the rest.

Part B premiums are also influenced by:

- Changes in healthcare costs (e.g., utilization of services, pricing)

- Enrollment trends

- Legislative changes

These factors can cause premiums to rise, sometimes more than general inflation or Social Security cost-of-living adjustments.

The following is a summary of the standard Medicare Part B cost changes from 2025 to 2026:

Income-Related Monthly Adjustment Amount (IRMAA)

Not every beneficiary pays just the standard premium. Higher-income beneficiaries pay an extra amount called the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is based on your modified adjusted gross income (MAGI) from two years prior (e.g., your 2024 tax return determines your 2026 IRMAA). IRMAA applies regardless of whether you are receiving Social Security benefits.

If your income is above certain thresholds, you pay progressively higher Part B (and Part D prescription drug) premiums. The more you earn, the higher the surcharge. Those brackets are adjusted annually for inflation.

Since IRMAA is based on income from two years prior, a higher-than-normal income year can result in higher Medicare premiums well after that income was received. As a result, Medicare costs may increase at a time when income has declined or stabilized.

2026 IRMAA Premium Ranges

Income-Related Monthly Adjustment Amounts (IRMAA) can increase the monthly Part B premium for higher earners based on their 2024 MAGI:

How Part B Premiums Can Affect Your Net Social Security Benefit

If you receive both Medicare and Social Security, Medicare Part B premiums are typically deducted directly from your monthly Social Security benefits. When Part B premiums increase, those higher costs can offset some (or in certain cases all) of the annual Social Security cost-of-living adjustment. As a result, even though gross Social Security benefits may rise year over year, the net amount deposited each month can remain flat or even decline.

This interaction can be an important part of retirement cash-flow planning, particularly as healthcare costs continue to evolve over time.

In Summary

Understanding how premiums are calculated can help you plan more effectively, especially if you’re nearing Medicare eligibility or navigating planning around Social Security income and withdrawals. Your Luminescent team can help evaluate individual circumstances for potential planning considerations, in coordination with your tax and healthcare advisors.

This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third-party sources and is believed to be reliable; however, its accuracy is not guaranteed and should not be relied upon in any way whatsoever. This presentation may not be construed as investment, tax or legal advice and does not give investment recommendations. Any opinion included in this report constitutes our judgment as of the date of this report and is subject to change without notice.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.