How Arizona taxpayers can redirect state taxes to causes they care about

Arizona taxpayers have a unique opportunity to redirect a portion of their state tax dollars to causes they care about without increasing their overall tax bill. The Arizona Tax Credit can be a powerful planning tool, allowing you to support qualified organizations while reducing your Arizona state tax liability dollar-for-dollar.

If you are an Arizona taxpayer, there is still time to take advantage of the Arizona Tax Credit for 2025. Contributions for the prior tax year may be made up until the April filing deadline.

A tax credit reduces your tax liability on a dollar-for-dollar basis. The Arizona Tax Credit directly reduces the amount of Arizona state income tax you owe for the year. Because these credits are nonrefundable, the total credit you can claim in a given year cannot exceed your Arizona tax liability.

This can allow you to potentially offset up to the full amount of your Arizona tax liability, regardless of the amount of tax you paid throughout the year. If you withheld an amount equal to or greater than your Arizona tax liability, the credit will increase your Arizona tax refund. Otherwise, it reduces your remaining tax liability. You may carry the unused credit forward for five consecutive years.

Example:

A married couple has an Arizona state tax liability of $5,900 for 2025. During the year, they:

- Contribute $4,900 to qualifying Arizona tax credit organizations

- Withhold $1,500 for Arizona state taxes

When they file their return, their tax liability is fully offset by the credit, and the excess withholding results in a $500 refund. In effect, they redirected $4,900 of their Arizona tax dollars to causes they care about.

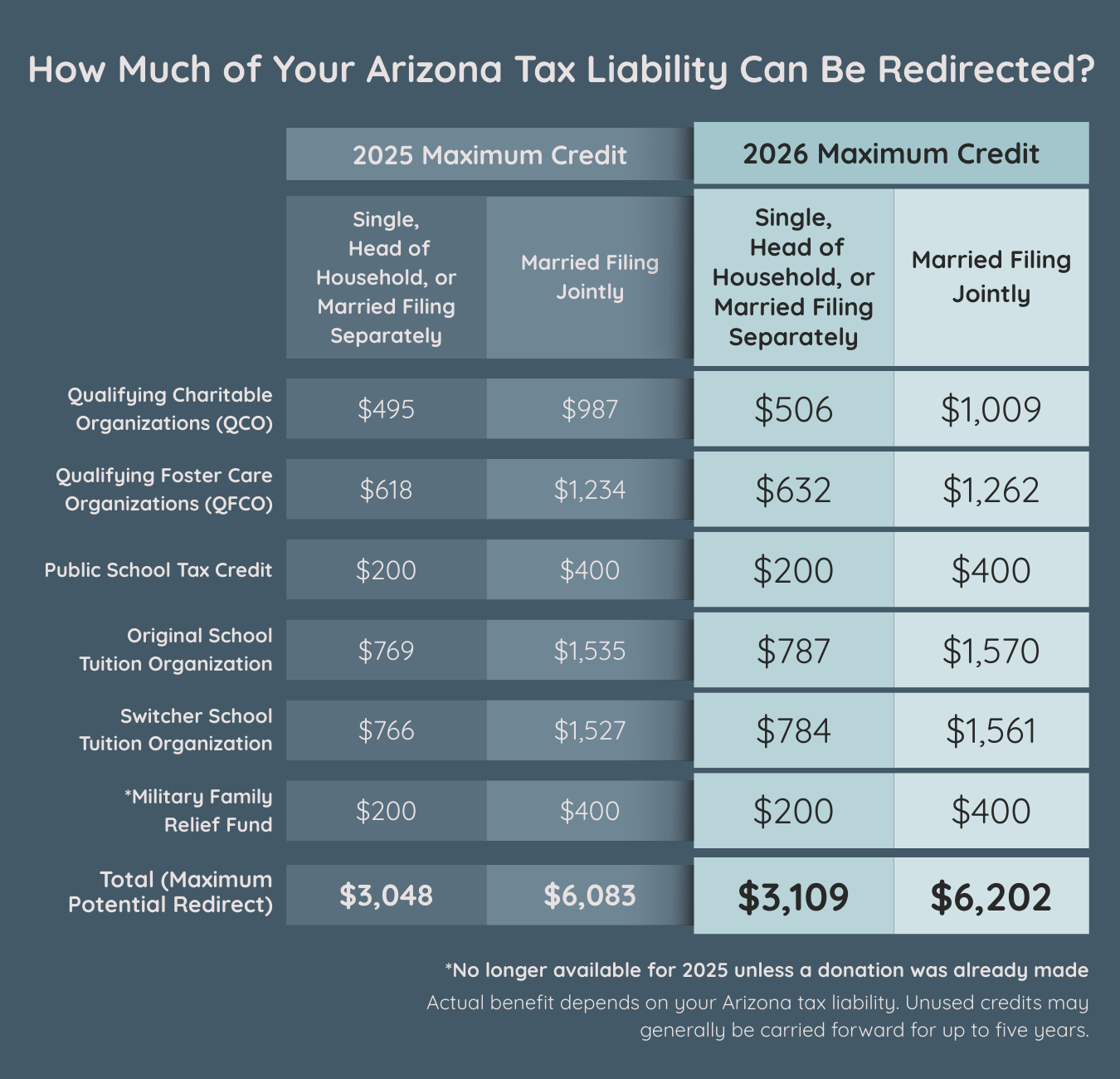

How Much of Your Arizona Tax Liability Can Be Redirected?

For 2025 and 2026, Arizona taxpayers may be able to redirect up to the following amounts of their Arizona state tax liability to qualifying causes:

Credit for Contributions to Qualifying Charitable Organizations (QCO)

This credit is available for contributions to Qualifying Charitable Organizations that provide immediate basic needs to residents of Arizona who receive temporary assistance for needy families, are low-income residents, or are individuals who have a chronic illness or a physical disability.

Credit for Contributions to Qualifying Foster Care Charitable Organizations (QFCO)

This credit is available for contributions to Qualifying Foster Care Charitable Organizations that provide services to qualified individuals in the Arizona foster care system, spend at least 50% of their annual budget on those services, and serve at least 200 qualifying individuals each year.

Public School Tax Credit

This credit is available for making contributions or paying fees directly to an Arizona public school for support of eligible activities, programs, or purposes as defined by statute.

Credit for Contributions to Certified School Tuition Organizations (STO)

There are two separate tax credits available to individuals for contributions made to a Certified School Tuition Organization, which provides scholarships for students enrolled in Arizona private schools.

Original STO Credit

This credit is available for individual taxpayers who make contributions to a Certified School Tuition Organization. The maximum credit amount is set annually and is claimed on Arizona Form 323.

Switcher (PLUS) STO Credit

This credit is available to individual taxpayers who first donate the maximum amount allowed under the Original STO Credit (Form 323) and then make an additional contribution to a Certified School Tuition Organization.

Credit for Donations to the Military Family Relief Fund

This credit is available for donations made to the Military Family Relief Fund, which is administered by the Arizona Department of Veterans’ Services. There is an annual cap of $1M in donations. Please note, this credit is no longer available for 2025 unless a qualifying contribution was already made, but you can potentially make a 2026 contribution.

Next Steps

The Arizona Tax Credit can be a valuable planning opportunity, allowing you to manage the timing of charitable contributions and potentially redirect a portion of your state tax liability toward causes you care about. Because individual circumstances vary, we encourage clients to contact their Luminescent team to evaluate how these strategies may fit into their overall financial and tax planning, in coordination with their tax professional.

This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third-party sources and is believed to be reliable; however, its accuracy is not guaranteed and should not be relied upon in any way whatsoever. This presentation may not be construed as investment, tax or legal advice and does not give investment recommendations. Any opinion included in this report constitutes our judgment as of the date of this report and is subject to change without notice.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.