“Patience is bitter, but its fruit is sweet.”

― Aristotle

Every market cycle has its ups and downs, but the long view often rewards those who stay invested. Volatility can test patience, yet it also reinforces the importance of a thoughtful, diversified approach. By maintaining perspective and balance, investors can stay on course regardless of short-term market noise.

This past quarter illustrated that progress often unfolds alongside uncertainty. Markets advanced amid solid earnings reports and accommodative policy developments, even as lingering risks created a more complex backdrop. While some investors may be cautious at current market levels, it’s worth remembering that new highs are a normal part of the market cycle, not necessarily a warning sign. Investors who maintained discipline benefited from remaining invested through the volatility instead of reacting to shifting headlines.

Stocks and bonds each contributed to portfolio stability during the quarter. Equities were supported by strong corporate results and improving sentiment, while bonds found their footing as inflation trends moderated and policymakers signaled flexibility. Together, these developments emphasized the value of maintaining diversification as markets adapt to evolving economic conditions.

The Fed continued to face the challenge of loosening policy enough to support growth while remaining vigilant against inflationary resurgence.

In September, the Federal Reserve lowered its benchmark rate by 25 basis points, which was the first cut of 2025. Inflation readings had cooled modestly through the quarter, giving policymakers room to act. Markets responded positively, possibly reflecting optimism that the easing cycle could extend into 2026.

While this was happening, public discourse over the Fed’s independence grew louder, raising concerns that future decisions may be scrutinized as much for optics as for economic rationale. However, heading into 2025, many analysts and rate-futures markets had already priced in the expectation that rate cuts would begin sometime in 2025. This was forecasted under the assumption that inflation would continue moderating. Additionally, history shows that the Fed has occasionally initiated easing cycles when equity markets were near all-time highs in an effort to sustain expansion rather than react to a collapse.

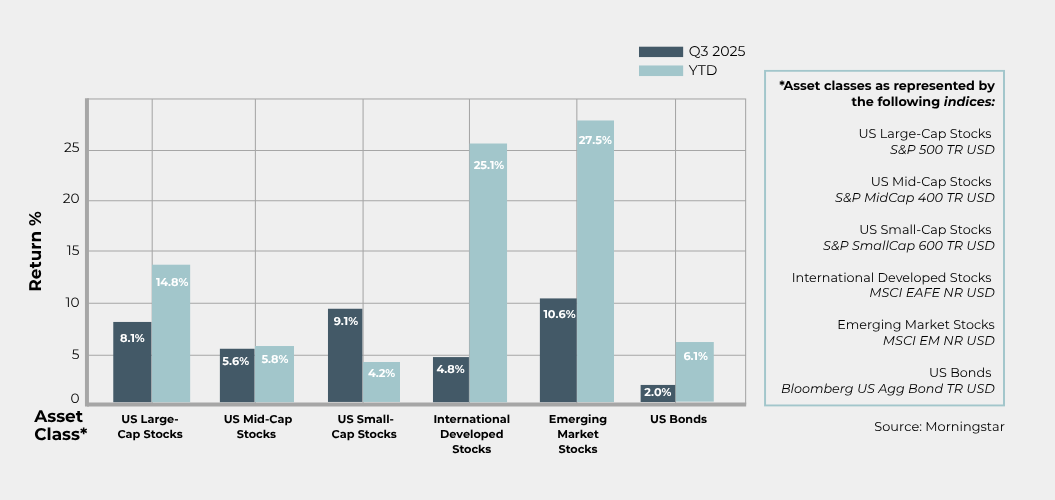

Corporate earnings continued to provide support for equities. Analysts are expecting the S&P 500 year-over-year earnings growth to be above 8% for the quarter. Technology, Industrials, and Financials were among the strongest contributors, and US Mid-Cap and US Small-Cap stocks benefited from the Fed’s rate cut.

Speculation around the corporate tax landscape turned into action with the enactment of the One Big Beautiful Bill Act (OBBBA) in July 2025, which provided companies and investors with clarity. The legislation made several key provisions permanent, offering businesses greater predictability in financial planning. This, in part, helped underpin the healthy earnings growth seen in the third quarter.

While valuations remained elevated, corporate earnings helped sustain investor confidence. The indication is that business conditions have held up better than many anticipated. The S&P 500 reached a record high 28 times year-to-date through September 30th, with 23 of those days occurring in the third quarter (Source: Yahoo Finance). These record-setting sessions highlight how solid earnings results contributed to market resilience.

Global trade policy continued to inject uncertainty into markets. While some tariff deadlines were postponed, new measures remained under discussion in sensitive areas such as semiconductors, steel, and pharmaceuticals. For many US companies, navigating higher input costs and adjusting supply chains likely added complexity to capital planning. These unresolved pressures contributed to more cautious growth forecasts across both developed and emerging markets. Meanwhile, emerging markets showed relative resilience, aided by a softer US dollar and capital inflows, though they remain exposed if trade tensions intensify.

The immediate impact on consumers has been relatively modest. While businesses are navigating higher input costs and adjustments in their supply chains, most households did not see major changes to day-to-day expenses. The phased approach to new tariffs and targeted exemptions has helped limit abrupt price increases, and many companies have been able to adapt gradually. As a result, while trade policy remains an important factor in market and business planning, its effect on consumer spending so far has been contained.

Consumer spending has shown a clear divide by income. Higher-income households remained relatively resilient, supporting overall growth, while lower-income consumers pulled back amid tighter budgets and rising credit stress. Housing costs, including slower new construction and mortgage rates that continue to weigh on affordability, have added pressure for many households. Consumer confidence surveys reflected this divide, with sentiment leaning more pessimistic even as aggregate spending stayed positive.

For most households, the immediate impact on day-to-day expenses has been limited. While some sectors face higher costs and supply chain adjustments, households have generally adapted without major disruptions. The overall picture suggests that, despite pressures on lower-income consumers, spending continues to support economic activity, though future trends may be shaped by how these financial pressures evolve.

Taken together, the events of the third quarter reinforce a few key takeaways. Markets showed resilience amid ongoing uncertainty, supported by strong corporate earnings, accommodative policy, and diversified investment opportunities. At the same time, risks remain unevenly distributed, as trade developments, shifts in consumer behavior, and debates over monetary policy could influence market conditions. Record-setting S&P 500 levels and solid earnings growth illustrate that, even in a complex environment, investors have seen areas of stability and opportunity.

Through it all, we remain committed to providing guidance and support, helping clients stay focused on their financial priorities even as short-term narratives evolve. Periods of volatility are an inherent part of markets. History shows that maintaining a disciplined, diversified approach can help investors navigate different conditions over time. Rather than trying to predict which theme will dominate next, portfolios can be structured to potentially benefit from multiple scenarios. By focusing on long-term objectives and aligning portfolios with individual goals, investors may benefit from potential growth while managing risk.

With political commentary intensifying, the Fed will need to reinforce its data-driven independence.

Corporate earnings growth remains solid, but valuations leave little room for disappointment.

Markets will be watching closely to see whether tariff disputes escalate or find resolution.

As the year winds down, it’s an ideal time to pause, review your finances, and identify any strategies that could help lower your upcoming tax

Originally published in the Journal of Accountancy 9/8/25 At Luminescent Wealth Management, we believe true financial stewardship means caring for every part of a family’s

This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third-party sources and is believed to be reliable; however, its accuracy is not guaranteed and should not be relied upon in any way whatsoever. This presentation may not be construed as investment, tax or legal advice and does not give investment recommendations. Any opinion included in this report constitutes our judgment as of the date of this report and is subject to change without notice.

The index and mutual fund performance shown is presented gross of our advisory fees, trading costs, and other expenses that may be incurred in an actual investment account. This information is provided for illustrative purposes only and does not represent the performance of any specific portfolio or client account. The index returns are not intended to imply or compare to actual portfolio performance and should not be relied upon as an indication of future results.

Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.