“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

― Benjamin Graham

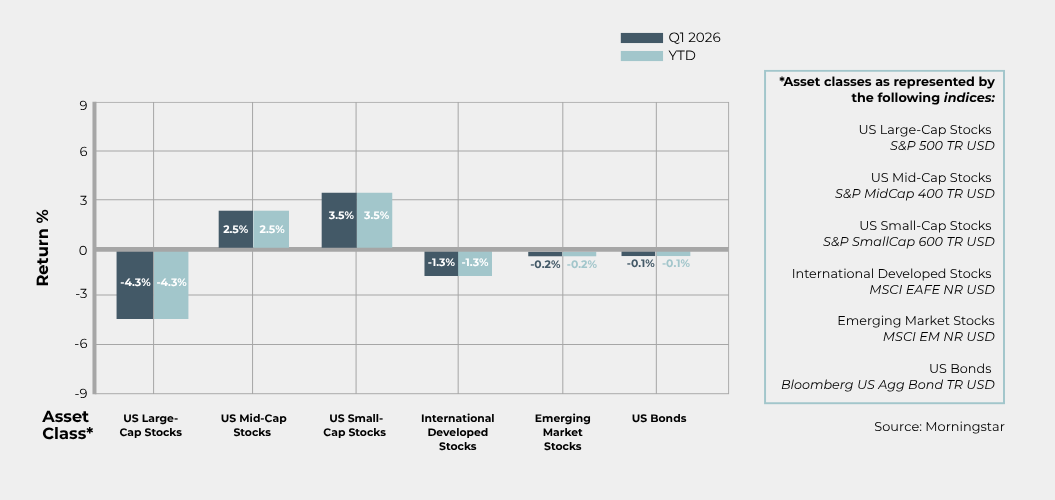

The first quarter of 2026 highlighted how quickly market narratives can shift. Entering the year, expectations reflected a broadly constructive outlook, supported by moderating inflation and the potential for a gradual easing in monetary policy. As the quarter progressed, however, a combination of economic data and external developments contributed to a more nuanced interpretation of the path forward.

Rather than a single dominant theme, markets responded to a range of inputs that influenced expectations in different ways. Inflation trends proved less linear, interest rate expectations adjusted, and geopolitical developments introduced additional considerations. This fostered an environment where changes in outlook were often incremental, but still meaningful in how they shaped asset pricing.

For investors, periods like this are a natural part of the cycle. Market outcomes are swayed not only by economic fundamentals, but also by what investors anticipate may lie ahead. The first quarter serves as a reminder that shifts in the narrative can influence market behavior, reinforcing the value of maintaining a long-term perspective and a disciplined strategy, particularly during periods of increased uncertainty. In this context, maintaining consistency in approach and a well-diversified portfolio can often matter more than reacting to short-term developments.

Geopolitical dynamics became a key driver of markets during the first quarter, shifting the narrative away from one primarily defined by macroeconomic trends and monetary policy toward one increasingly shaped by external events. While the year began with a focus on growth and the expected path of monetary policy, developments across multiple regions introduced new sources of uncertainty with more direct economic implications.

Early in the quarter, developments in Venezuela raised questions around the stability of energy production and export flows, contributing to incremental tightening in global supply expectations. Around the same time, renewed attention on Greenland brought trade relationships, resource access, and strategic positioning back into focus. While these dynamics did not result in immediate market dislocations, they contributed to a gradual increase in perceived geopolitical risk.

As the quarter progressed, conditions in the Middle East marked a more meaningful inflection point. Developments involving Iran introduced uncertainty around key energy transit routes, including the Strait of Hormuz, and broader supply continuity. This contributed to rising oil prices and increased volatility within energy markets, alongside more noticeable fluctuations across financial markets and a more cautious tone in investor positioning. In Europe, energy security considerations and lingering supply chain sensitivities added to the broader multi-regional nature of these pressures.

Importantly, these events unfolded sequentially, leading to a cumulative repricing of geopolitical risk rather than a single-point shock. The resulting shift was reflected across asset classes, with energy prices moving higher and broader financial conditions becoming somewhat more constrained. The progression from localized developments to a more systemic influence reflects how quickly geopolitical factors can become macro-relevant considerations.

From an economic standpoint, the significance of these dynamics lies in their transmission channels. Higher energy prices feed directly into inflation both through headline measures and via production and transportation costs. At the same time, elevated uncertainty can weigh on business investment and hiring decisions, while also influencing consumer sentiment. In parallel, renewed focus on supply chain reliability highlights the potential for disruptions to affect both pricing dynamics and growth outcomes.

While geopolitical factors are inherently difficult to forecast, markets have typically demonstrated an ability to adjust as conditions stabilize. Although these factors can influence inflation, growth, and financial conditions in the near term, their effects are often more limited over time. The experience of the quarter points to a broader pattern: headline events tend to matter less as isolated shocks, and more in how they accumulate and gradually reshape how markets perceive and price risk.

Energy markets were a key area of focus during the quarter, with prices moving higher as supply expectations tightened. These dynamics were reflected in energy markets and inflation data, and were also increasingly evident in everyday price pressures, including at the gas pump. This followed a period of relative stability in late 2025 and introduced renewed variability into a component of inflation that had been moderating. As a result, rising energy prices contributed to upward pressure on headline inflation and raised the potential for broader pass-through effects, particularly if sustained.

These dynamics influenced the path of inflation and, in turn, expectations for monetary policy. Entering the year, consensus generally pointed toward a gradual easing cycle. Over the course of the quarter, however, those expectations adjusted as inflation showed signs of stabilizing above long-term targets, contributing to a more measured outlook for policy.

From a market perspective, the effects were felt across asset classes. Fixed income markets experienced upward pressure on yields, while equities faced some valuation headwinds as discount rates adjusted. While the impact was not uniform, the environment led to more pronounced dispersion across sectors and asset classes, as markets responded to a more uncertain inflation and policy backdrop.

Labor market conditions remained a source of underlying strength during the first quarter, even as monthly data exhibited notable volatility. Employment gains were strong at the start of the year, with January adding a solid number of jobs, before softer conditions emerged in February amid a temporary pullback in hiring. The labor market then rebounded in March, with job creation accelerating and offsetting the prior month’s weakness.

Despite this uneven monthly pattern, employment conditions remained broadly steady. Sector trends were uneven, with healthcare continuing to lead hiring while other areas were more mixed. Overall, hiring activity continued to support household income and consumption, while layoffs remained relatively contained, reflecting a labor market operating in a low-unemployment environment with sustained labor demand.

Rather than being defined by individual monthly fluctuations, the labor market backdrop over the quarter was characterized by steady employment conditions and persistent job creation. Low unemployment and consistent hiring provided a steady anchor for the economy, supporting positive economic momentum through the period.

As the first quarter demonstrated, market environments are often shaped as much by evolving expectations as by underlying economic conditions. While the path of inflation, interest rates, and external developments proved less linear than initially anticipated, the broader framework for long-term investing remains unchanged.

Periods of adjustment are a natural feature of market behavior and reflect how expectations are refined over time. Rather than responding to each shift in isolation, outcomes are better understood through how incremental changes build into broader trends. As these dynamics unfold across different parts of the market, they also reinforce the role diversification plays in portfolios.

Maintaining perspective and avoiding overreaction to short-term shifts remains an important component of a disciplined approach. Periods of volatility or temporary weakness are a normal feature of long-term investing.

Our approach remains centered on thoughtful planning and a consistent decision-making framework aligned with long-term objectives. While conditions may change over time, they do not alter the importance of making measured, deliberate decisions in pursuit of those objectives.

Developments in the Middle East will remain a key focus, particularly for their potential to influence energy prices and near-term inflation dynamics.

The policy outlook is expected to remain data-dependent, with the timing and pace of any adjustments shaped by the interaction between inflation persistence and signs of moderating growth.

Inflation may increasingly be driven by services and wage-related pressures, even as energy prices continue to influence shorter-term readings.

The current uneven distribution of job growth across sectors will be monitored for signs of broadening or rebalancing in upcoming quarters, and what that may signal for overall labor market momentum.

Springtime brings warmer weather and spring cleaning. It’s a natural time to reset, not just at home, but in your financial life as well. By

We’ve always believed that growth should be intentional. We don’t think of growth as getting bigger for the sake of it. For us, it’s about

Originally published on The Street. Financial planner Erin Itkoe breaks down Arizona’s flat tax, Social Security rules, and retiree-friendly provisions. Erin was recently featured in